For: ePURE – the European renewable ethanol association

[January – May 2022]

The European renewable ethanol association (ePURE) would like to understand the position of bio-ethanol compared to various renewable fuel and drivetrain options for climate action in the passenger car segment. This based on their greenhouse gas emission abatement costs; how do these abatement costs change over time; and how fast and easy can these options be deployed to reduce climate emissions, so to reduce climate emissions from transport as soon as possible.

Therefore, we evaluated the carbon savings achieved by, and the costs of six types of powertrains and three types of renewable fuels at various blend fractions:

- Petrol car driving on E10, E20 and E85 blends of renewable ethanol

- Diesel car driving on a B30 blend of biodiesel, and B100 (FAME) or HVO100 (100% renewable diesel)

- Gas car driving on compressed biomethane

- Mild hybrid electric vehicle driving on E5, E10, E20 and E85 blends of renewable ethanol

- Plug-in hybrid electric vehicle driving on E5, E10, E20, E85 blends of renewable ethanol in combination with 100% renewable or average grid electricity

- Two types of battery electric cars driving on 100% renewable or average grid electricity

In our study, we assessed the greenhouse gas abatement costs of these options before policy intervention, so that the abatement costs represent the total costs for climate emission savings for consumers and government together. Based on the understanding of the true costs, governments can decide on what options are best stimulated and shift the burden by means of subsidies, taxes and other policy instruments.

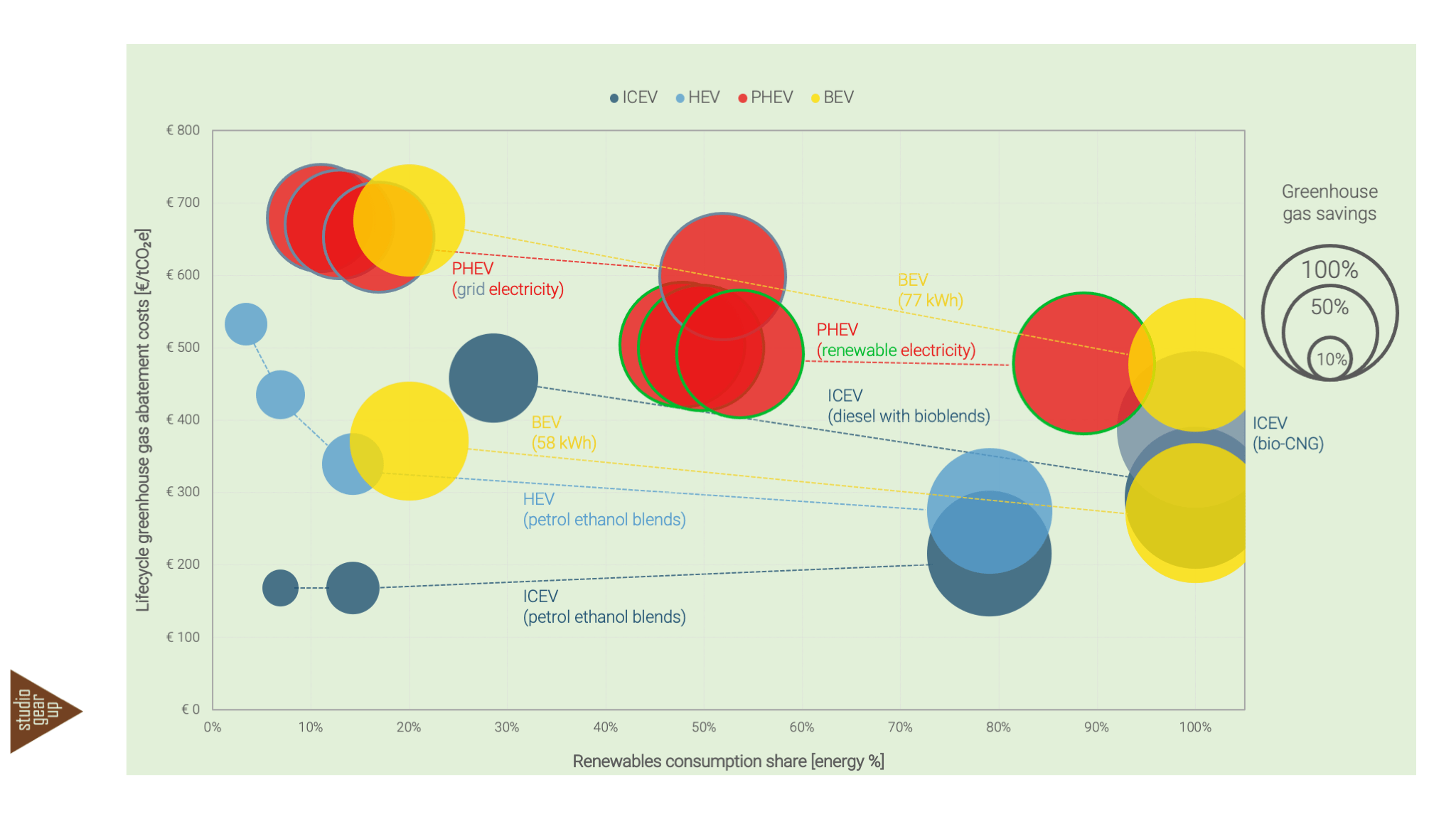

Figure 1 below shows that renewable ethanol, in blends ranging from E10 to E85, has low greenhouse gas abatement costs compared to switching to other fuels or drivetrains. Blending in ethanol is the most cost-effective option, but with relative modest climate reduction. This is due to blend walls, in most national markets max 10% blending levels. However, 10% ethanol is on the level of the vehicle park the most-cost effective climate option.

Figure 1. The amount of greenhouse gas savings and abatement costs per option, as a function of the share of renewable energy. The size of the balls represents how much greenhouse gas emissions the options are saving. The x-axis represents the renewable share in the energy used by the vehicle, and this allows to understand how options improve when the fraction of renewable electricity in the grid increases, or when higher blends of renewable fuels are used. The y-axis represents the abatement costs. Emission savings are based on the observed performance in the EU market. Energy costs are based on the average in the EU between January 2019 and January 2021. Vehicle costs are based on purchase prices in January 2022, and a use of 20 years and 250,000 km.

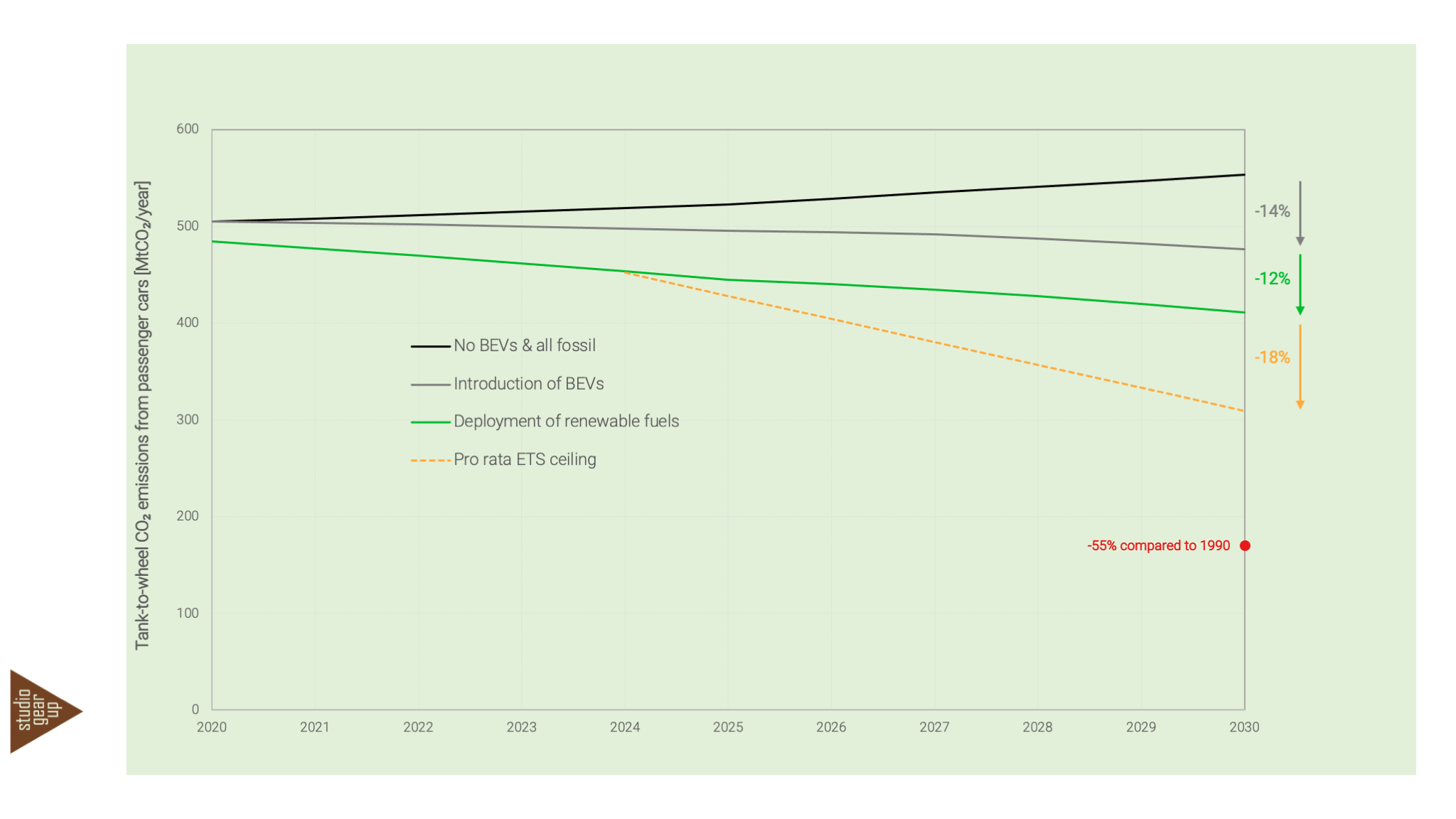

When assessing the combined effect of proposed European policy measures, we conclude that the CO2 emission performance standard – stimulating the introduction of electric vehicles – and the proposed RED III target to reduce the emission intensity of fuels, together do not achieve enough greenhouse gas emission reduction to get on track to climate neutrality in 2050, see Figure 2. Actually, higher volumes of renewable fuels would be required to reduce emissions in the current (and remaining) fleet of internal combustion engine vehicles.

Figure 2. Tank-to-wheel emission development in the transport sector, and how emissions decrease thanks to the introduction of BEVs and renewable fuels. The achievement is compared to a possible ETS trajectory for road transport and buildings, and the economy wide -55% target of the Fit-for-55 policy package, both assuming that passenger cars would contribute pro rata to a required overall emission reduction in the transport sector and the ETS for road transport and buildings.

Other policy measures could further increase the demand for renewable ethanol. The Energy Taxation Directive could help to translate the attractive carbon abatement costs to an attractive pricing of ethanol fuel for the consumer. The Effort Sharing Regulation will force Member States to accelerate climate action in all sectors of the economy and as options in other sectors become exhausted, the focus will increasingly be on transport.

However, such an increased role of renewable ethanol in climate action in the petrol passenger car segment would require:

- That the sector maintains the cost-effective position of high ethanol blends by sustainably increasing the production volumes. Enough supply of alternative fuel volumes in the market lead to cost-effective options for end-users.

- The supply of ethanol above the caps (that limit the contribution of food and feed crop-based ethanol blends) by investing in the production of advanced ethanol. The sector should demonstrate the renewable ethanol industry’s ability to produce from Annex IX A feedstocks and to contribute to the minimum Annex IX A targets set by the Renewable Energy Directive, and beyond.

- Introduction of higher ethanol blends in the passenger car segment, which can cost effectively reduce emissions of the passenger car market. It is recommended to have a E10 blending mandate across Europe and a gradual phasing in of E20.

Read more in the press release of ePURE.

The report can also be downloaded here: